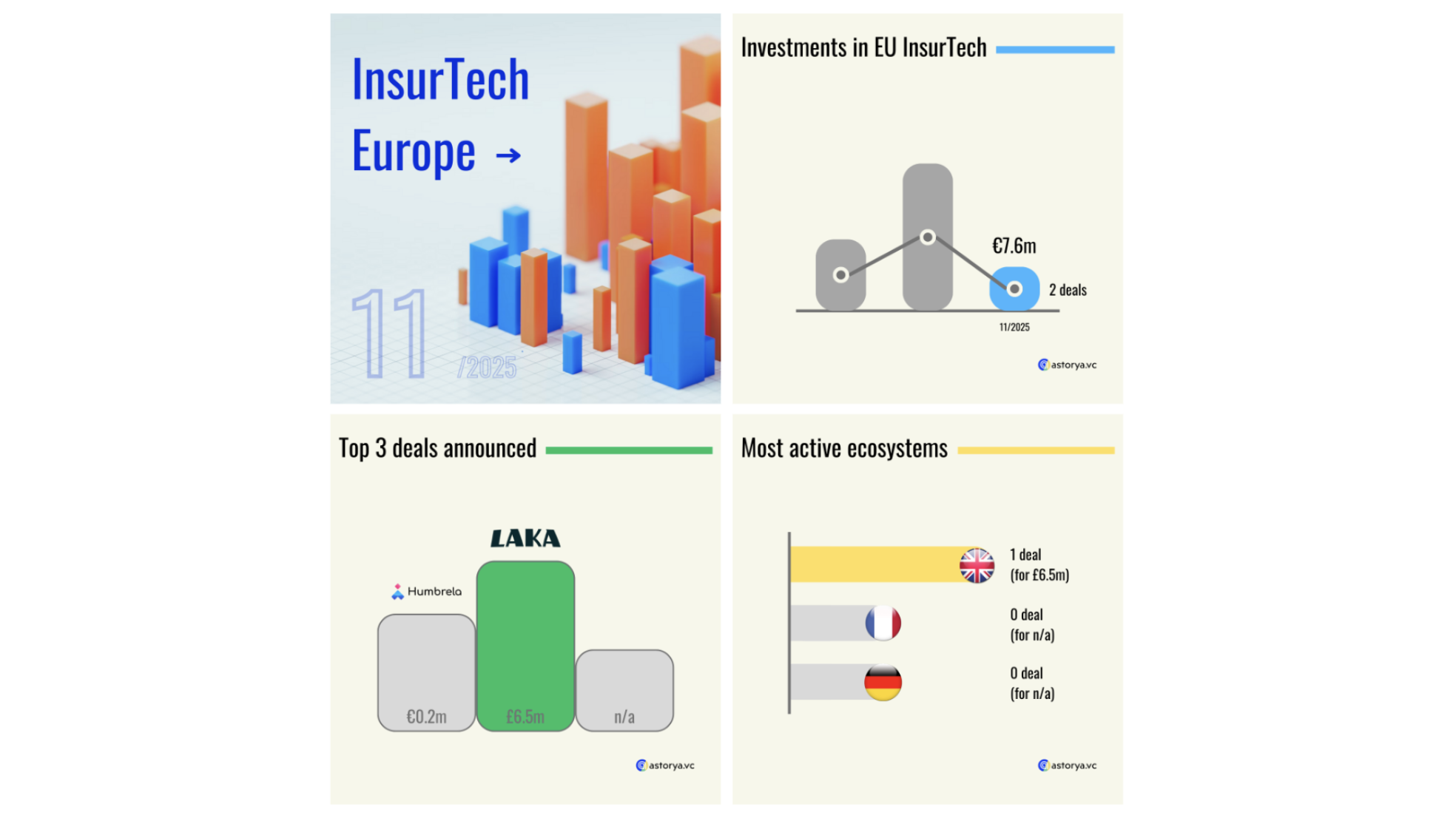

Despite a quiet November—perhaps a reaction to an unusually active October or anticipation of year-end surprises—European InsurTech deal volume since January is still up 5% year over year, even though total funding has fallen 27% as investors prioritize disciplined, revenue-driven “profitable growth” over the previous “growth at all costs” mindset. Capital is shifting away from cash-hungry full-stack carriers and B2C models toward more efficient plays across the value chain, which helps explain the lower invested amounts. November also highlights two key trends shaping the sector in 2024: the rise of AI, with startups either co-building broad solutions with insurers or offering targeted, ROI-driven tools despite long sales cycles; and the emergence of leaders within traditional InsurTech categories, exemplified by a B2C bicycle-insurance startup extending its Series B and mirroring other D2C players that are capturing scarce capital thanks to proven models and sustainable growth.

In short: 2 deals announced, 8m€ invested — that’s the headline.

Subscribe to our newsletter:

Let’s now take a closer look at the two most significant deals to see what insights they may reveal, either about the startup itself or about the broader trend they illustrate.

Let’s start with Humbrela, in second place. The Swiss startup announced a funding round of €161,000. Launched this year, the company claims to use artificial intelligence technologies to support brokers, agents, and MGAs. Its website highlights a focus on reducing administrative tasks through technology, therefore improving operational efficiency. In particular, the startup promises clients the ability to process more insurance policies in parallel thanks to the automation of many day-to-day tasks. This first round is led by Venture Kick, an initiative that invests in projects coming out of Swiss universities. On LinkedIn, it lists 8 employees, a number up 167% year-on-year.

Finally, at the top of the podium is Laka, which announced an extension of its July Series B, for a total of £6.5m. The UK startup turned to venture debt from HSBC, seemingly confirming that its growth model is profitable enough to be financed through debt as it continues to scale. As a reminder, the company has been operating in bicycle insurance since 2017. It distributes largely online or through distribution partnerships with cycling brands and retailers. Beyond its home market, Laka operates in nine European countries, including Germany and France. In France, it notably acquired several operations, including Luko’s scooter insurance portfolio and the e-bike specialist Cylantro. Also worth noting is its collaborative model, in which actual monthly claims are shared across the community, making the cost variable for each member but never exceeding a predetermined cap. While Laka doesn’t disclose precise figures — neither in policy count nor premiums — it lists 143 employees on LinkedIn, a number up 21% year-on-year.