Every six months, we put together facts and figures about the European InsurTech ecosystem. This is based on every deals announced in that space, our own market watch and scouting - enabled by our proprietary & automated scouting tool.

Below is a summary of the webinar we ran earlier this week, to detail KPI, major trends and what we expect next. You can watch it in replay, here.

You may have read it a lot last year: "investments are down". But the investment dynamic is slightly more complex, especially in the InsurTech industry.

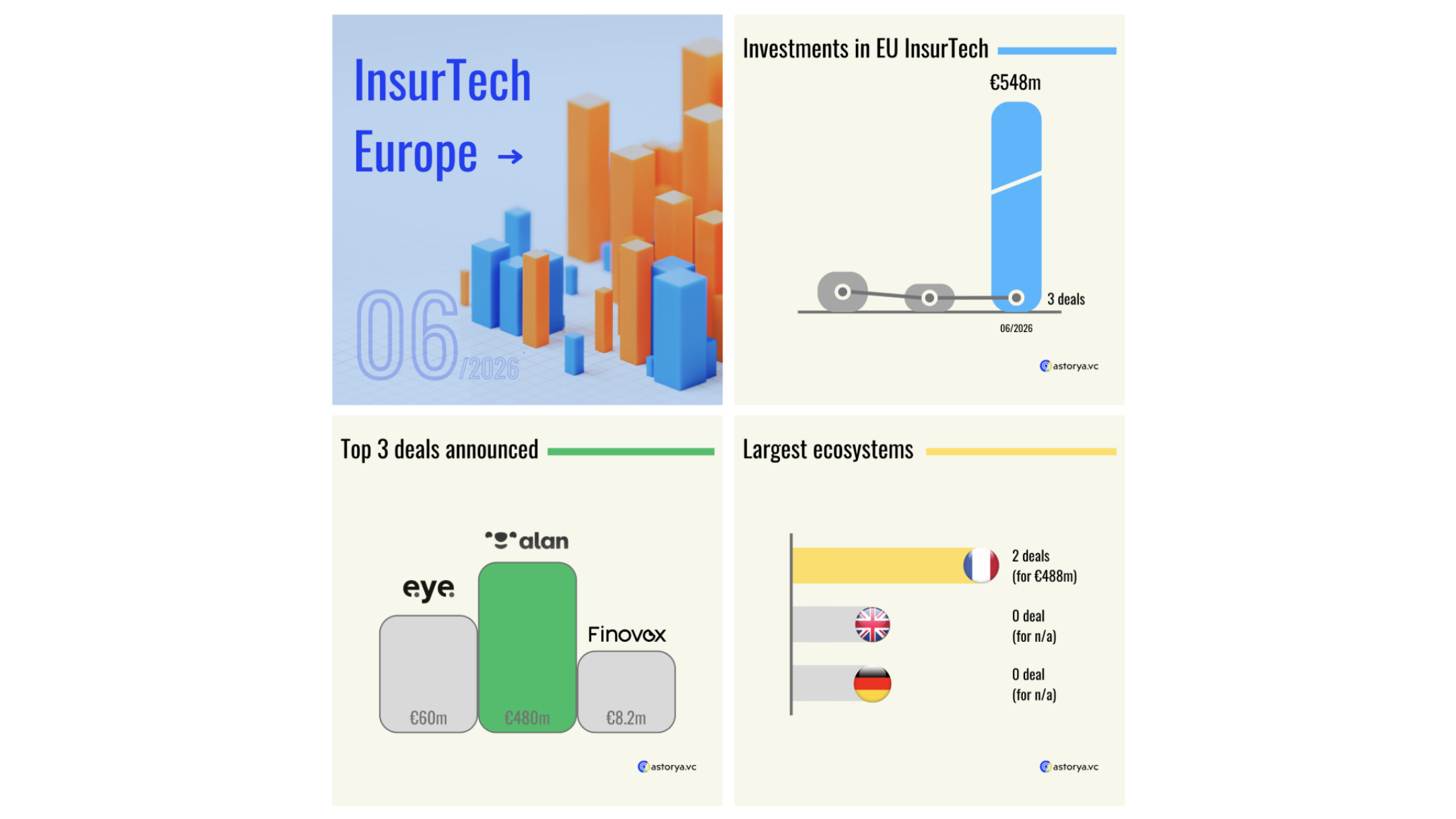

With 61 deals announced last year, this is indeed a drop from a year before.

But over €820m were invested in the European InsurTech ecosystem last year, which is up from a year before.

In addition, the chart displaying InsurTech investments across Europe over the last year (see the left part of the picture below) seems very similar to the one tracking all VC investments across European industries (see the right part of the picture below), or the one on FinTech investments worldwide, or even the one monitoring any VC investments across the world in the last year.

This trend, down from the peak time, is not specific to the InsurTech industry !

Subscribe to our newsletter:

And Q3 2024 was the hottest in a while, with massive rounds back to the market (kudos to Alan and Akur8 - both announced in France - which raised over €100m rounds !)

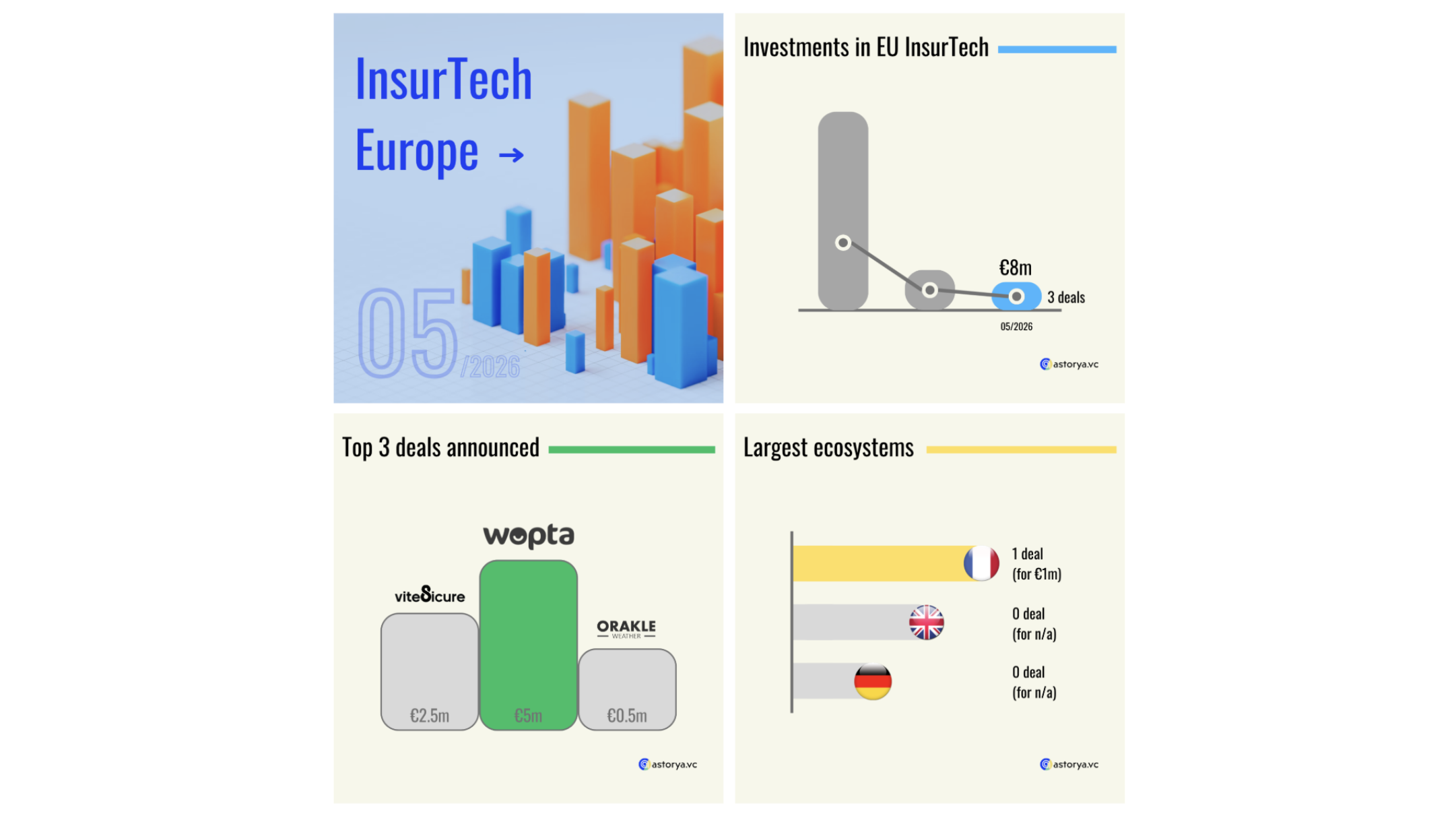

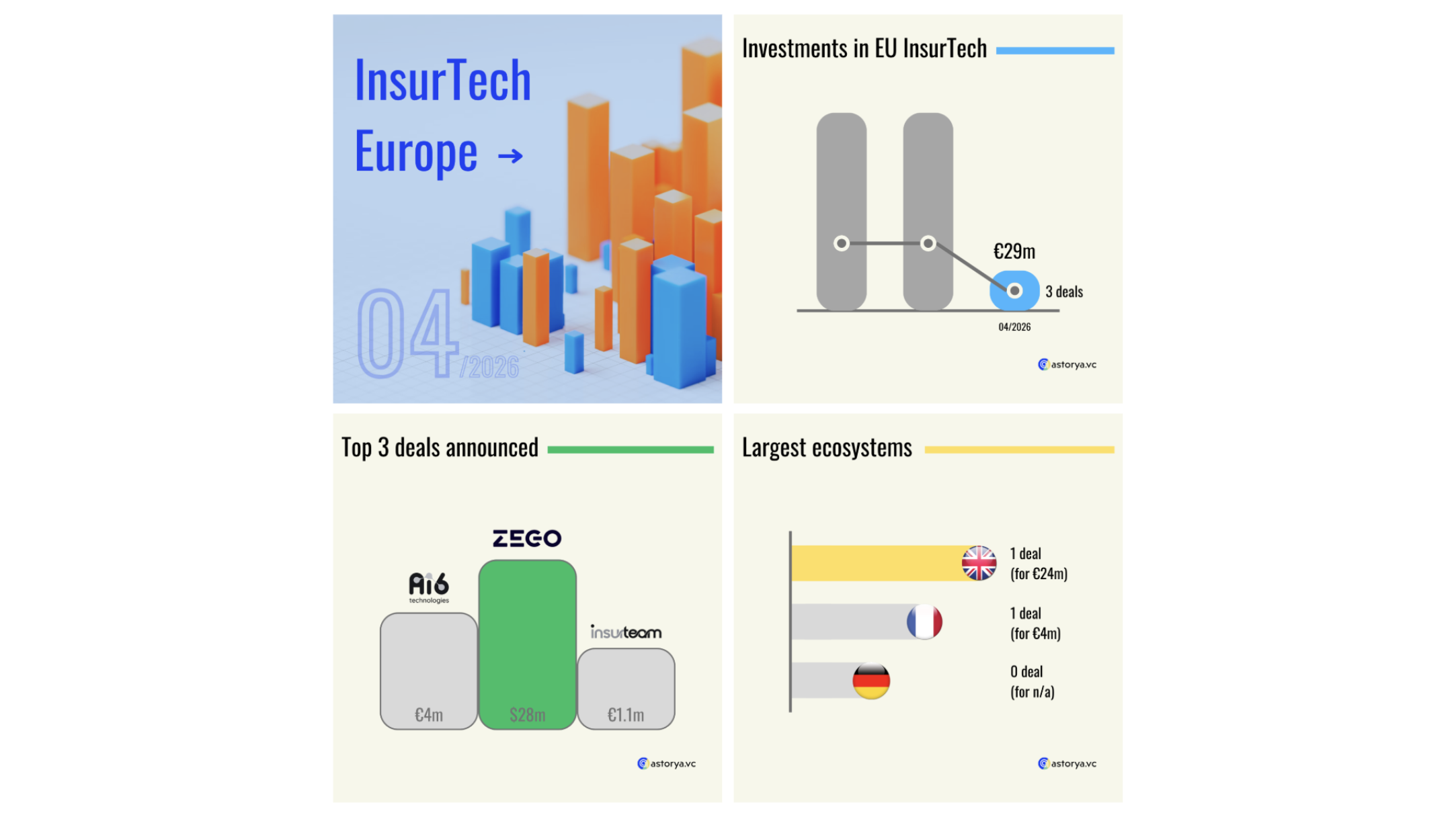

This enabled the French InsurTech scene to be the largest one in terms of money raised, while the UK remained the first one in terms of deal activity. Once again, Germany lagged behind with only a third and slightly more than a forth of all deals announced respectively in France and in the UK !

Outside of these three largest startup ecosystems in Europe, local ecosystems remained active. And 25% of all deals were announced in this "Rest of Europe". The Swiss market led the wave while Spain remained at high level. Note that many of these rounds were raised by startups operating in the "emerging risks" category. We’ll come back later on to that topic.

Beyond the investment dynamic which has changed since the post-pendemic era, the ecosystem mindset has changed too: the "growth at all costs" era is over and investors are increasingly speaking - and looking for - "profitable growth". In that background, several startups have announced they had achieved such a milestone: Mila and Acheel in France, Clark in Germany - note that this is the only unicorns which has made such an announcement as we speak - Cuuva in the UK and EIR in Sweden.

***

Beyond these names, there are other players which didn’t announced it yet. And there are players which are not profitable yet. The challenge for the most mature startups is that they need to have a profitable insurance portfolio (for those selling insurance products), make sure their sales cycle is profitable - that’s the famous CAC/LTV ratio VC often refer to - and ultimately they can expect to be profitable at the company level.

While many delayed their cashwall last year either with internal rounds (bridges led by existing investors) or by reducing their spendings with smaller teams, several M&A deals were inked. Acquirers either purchase a tech stack or focus on the insurance portfolio. Note that Allianz Direct was the most active acquirers with Luko, iptiQ (SwissRE’s former Embedded Insurance initiative) and Friday (Baloise’s former intrapreneurship InsurTech).

***

The change of mindset mentioned above is one reason explaining a persistent trend we perceived last year: CEO resigning. In 2024, ten InsurTech companies publicly announced such a move, including several unicorns: Wefox, Manypets, Clark and Tractable.

***

These unicorns have enjoyed a mixed dynamic since the peak time. In terms of team size: two kept growing, three remained relatively flat and three faced a significant drop over the last two years.

Note that this is only a public proxy (figures are available on LinkedIn) of their business dynamic. The counter example being Klarna in the FinTech space: they announced great business KPI recently, while a fourth of their team was slashed !

While "AI is eating the world" as many articles refer to, TechCrunch mentioned that 25% of funds invested last year in the European startup scene went to AI-first companies. In the InsurTech space only, 30% of euros were raised by AI-first players. As one round was over €100m, it’s worth having a look at the number of AI rounds in InsurTech: 18% of all rounds were inked by AI-first InsurTech startups last year.

In addition, there are several trends supporting the case of expecting more "AI in insurance" in the near future. As Accenture reported a few months ago, insurance is among industries expected to be impacted the most by AI. Several funds - including Bessemer Ventures - predicts AI to increasingly turn vertical. Others - including Pont Nine - expect the SaaS environment to be accelerated with AI. Several - including A16Z - consider Agentic AI as the next RPA, which we believe could unlock a clear wave of automation in the insurance industry.

***

Embedded Insurance has long been discussed while several data points show the momentum is finally here. Beyond funding rounds - Neat announced a massive €50m deal this year - we saw platforms adding insurance to their offer. Qonto recently added a real embedded insurance offer, which customer can access directly in Qonto’s own market place. Ornikar is another example, showing it’s not a matter of ‘if’ but ‘when’ embedded insurance will happen: back in 2019, we listed Ornikar - an online driving school - as a relevant platform when it come to embedding insurance (car insurance in that example). In January 2021, it did launched an insurance offer, focusing first on young drivers. Six months later it expanded it to any kind of drivers. And most of all, last year, it started selling… home insurance !

And beyond, there is a pattern: platforms increasingly add Financial Services to their line of products (Shopify, Grab, etc) and insurance is often the latest one to be embraced.

***

Last year the ‘product’ section of the value chain was very active - compared to years before - and in that category, many startups were tackling "emerging risks". They accounted for 20% of all deals announced and most remain in their early days (accounting for 15% of all euros invested in InsurTech Europe).

There were three major categories active last year in that space: Cyber InsurTech, startups enabling carbon credit insurance and those tackling climate-related risks (this includes the long-discussed ‘parametric insurance’ sector).

While more startups are raising on these topics, it’s worth highlighting incumbents are increasingly talking about these "emerging risks". Beyond AXA and Allianz famous risks report, more local players - like CNP - or reinsurance players - including SwissRE and MunichRE - regularly release reports detailing these risks and threats.

And we strongly believe this is were technology, data and algorithms could help a lot. Hence, startups are well positioned to develop solutions incumbents could rely on to unlock risk carrying.

Overall, we’ll increasingly invest in that category and will soon announce a deal in that space btw. Stay tuned ;)