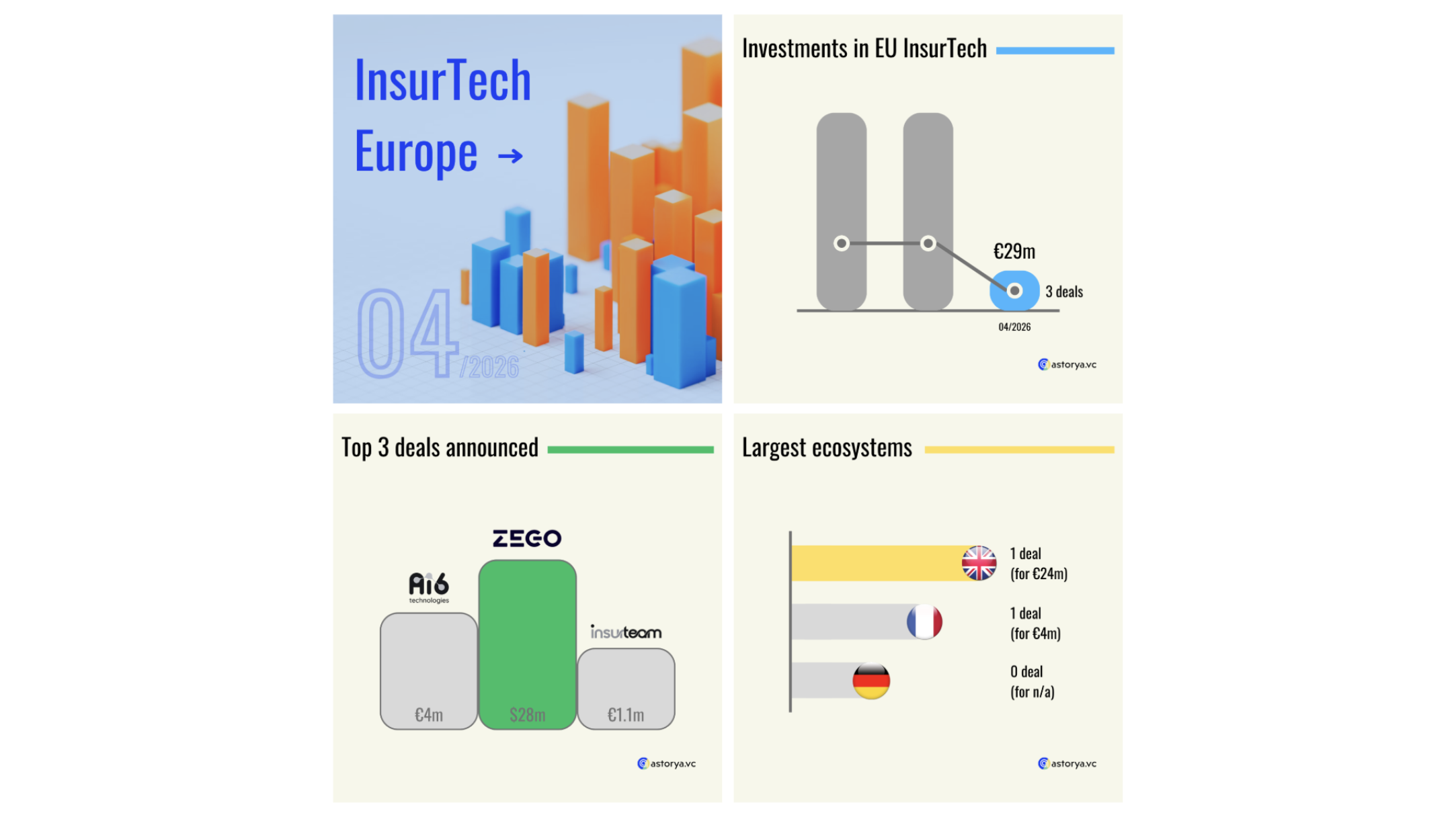

April saw a mixed activity. Only 4 deals were announced in recent weeks, making it the lowest monthly level since the beginning of the year. However, €72 million was invested in Europe, almost at the same level as the previous month. So, you'll quickly figure out, it's a few rare but significant rounds that animated the InsurTech scene.

In short, 4 deals announced, with €72 million invested, that's what you need to remember in terms of numbers.

This month, Element announced the largest round with €50 million raised. If you're familiar with the InsurTech scene, you definitely know this German startup. Launched in 2017, it falls into the category of "full-stack" players, meaning it has its own insurance license. Operating from the start on several property and casualty lines, it now claims 20 different products, covering auto, home, bike, and pet insurance. Initially launched with a direct distribution model, if I recall correctly, it now mainly relies on a B2B2C model and states on its website that it has signed over 70 distribution partnerships. In its communications, it claims the position of Insurer-as-a-Platform.

Element raised €50 million mainly from Mundi Ventures, which is entering the capital, alongside historical investors including a German pension fund. You may recall that the pension fund entered the capital during the Series B round, announced in mid-2022 for €21 million at the time. The dynamics of this new round are therefore rather positive: more than double the last time, and less than two years later. Especially in the market context that you are familiar with if you regularly follow this podcast - a rather calm market, to sum up. So, this round is significant. It's also the second largest since the beginning of the year! However, a German media outlet, Handelsblatt, indicates that the startup was actually looking to raise €100 million. Twice as much. That said, since its launch, the startup has still raised nearly $180 million!

Subscribe to our newsletter:

It's worth noting that on the occasion of this funding round, the startup shared some figures about its activity. In 2023, its premium volume surged by 150% to reach €50 million in premiums. By comparison, it announced a little over €10 million in premiums for the year 2021. Finally, you may recall that the founder of the startup stepped down and was replaced by a new CEO with extensive experience in the insurance sector, notably within the AXA Group. The announcement was made in July 2022.

The second significant deal this month concerns Pula, a Swiss startup offering parametric insurance solutions, notably targeting farmers. Launched in 2015, the company raises $20 million to further develop its offerings, particularly targeting Africa and Latin America. It claims to cover more than 15 million farmers through its offerings, across 22 different countries, generating a total of $80 million in premiums! The round is led by BlueOrchard, which invests notably in sustainable development issues in emerging countries. The Bill & Melinda Gates Foundation and Hesabu Capital also join alongside historical investors.

Finally, let's note the fundraising of the startup Estaly. Based in France, it announces a round of €3.6 million to accelerate the deployment of its Embedded Insurance solution. Launched in 2022, the startup allows eCommerce players and platforms to add insurance offers to their customer journeys. It claims to have more than 300 partner merchants to date. Furthermore, it highlights its DNA combining insurance and technology, but also retail since it targets actors of all sizes. Finally, it indicates already operating in Belgium, beyond the French market. And it relies on several insurer partners for its expanded product range: from mobility (bicycles or soft mobility), to housing (furniture, computers), to well-being (glasses and hearing aids). An interesting positioning, as it complements other players in the embedded insurance market operating in France.