Every six months, we share our analysis on the state of insurance innovation.

This bi-yearly review goes a bit beyond pure InsurTech to cover startups building resilience. We indeed believe there is a massive opportunity for data, algorithms and SaaS to tackle emerging risks !

You can watch our live conference here or read our summary below.

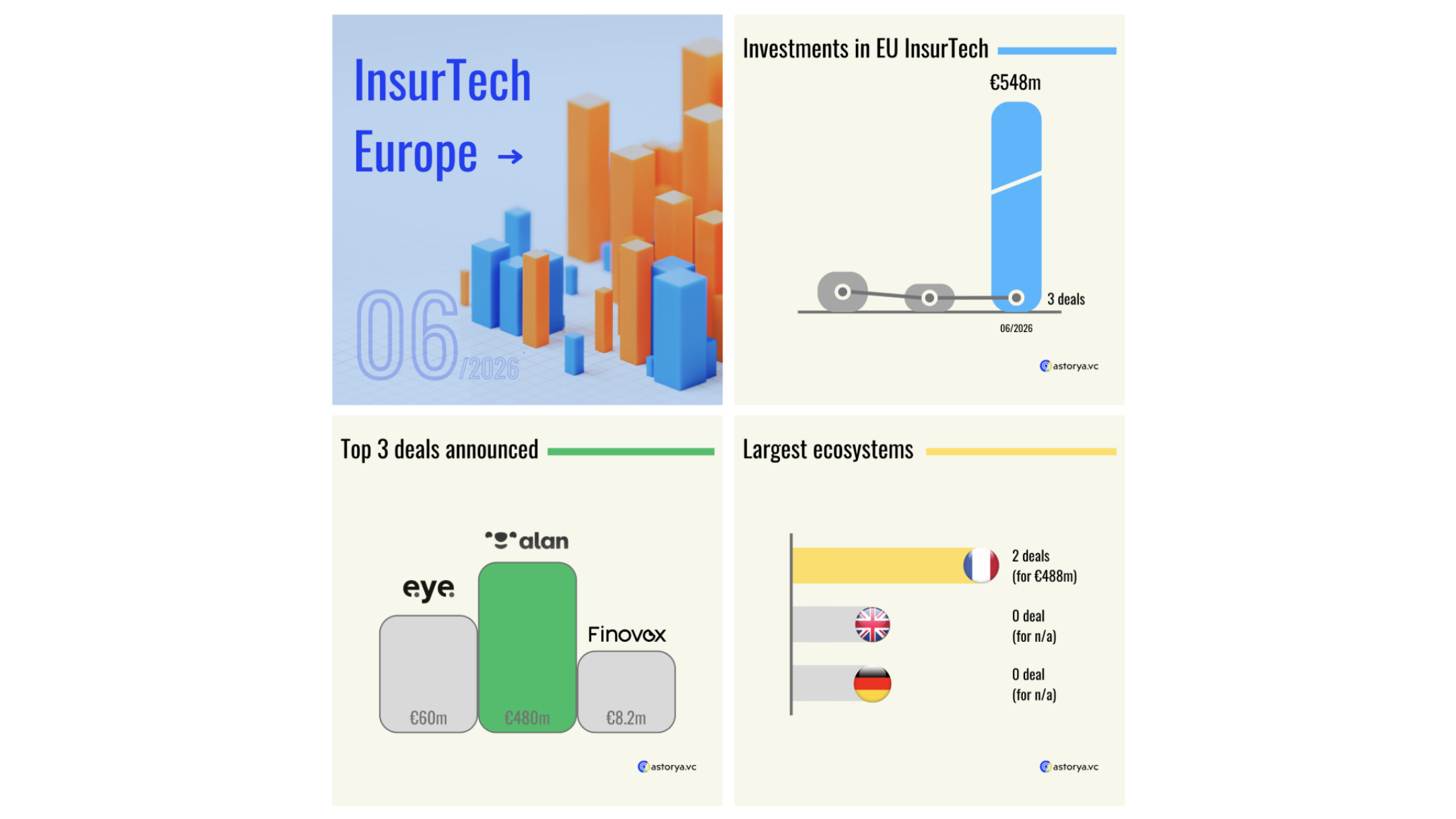

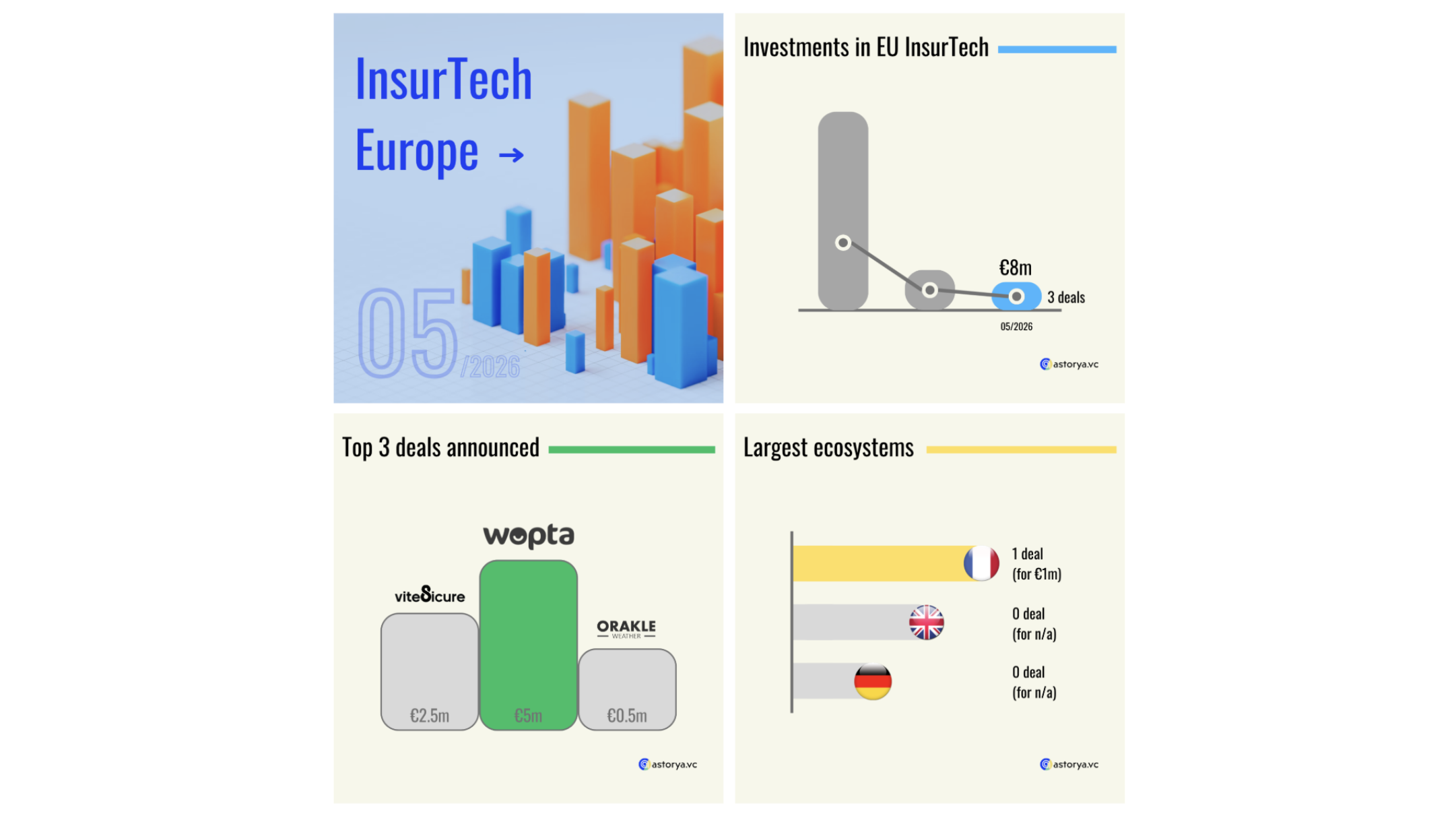

In the first half the year, 33 InsurTech deals were announced across Europe. All together, they raised €279m.

If you regularly follow our analyses, you may remember that depending on how you measure the investment activity, the dynamic might be different. It’s the case once again. The number of deals announced is indeed flat compared to the first half of last year (2024) while money invested in significantly down (-18%) compared to a year earlier.

And beyond pure InsurTech, we managed to track every deal announced in the French startup scene (thanks to Avolta Partners' weekly deal review). Based on this exhaustive data set, InsurTech accounts for ~10% of all deals related to emerging risks.

Applied to the European ecosystem, this would lead to 2.8B€ raised by startups building resilience across Europe !

In addition, it’s worth mentioning that several deals were not disclosed. One of them, Descartes Underwriting might be significant and could have boosted figures for the first half of this year.

Anyway, there were nice rounds announced in the first half of the year, with Marshmallow leading the wave with its B2C car insurance offer in the UK. Note that direct distribution enjoyed a kind of recovery with several deals announced with such a business model: Marshmallow, Orus, Dalma., Napo Pet Insurance, Ominimo Insurance . This highlights the first wave of insurance innovation - aka InsurTech 1.0 - is maturing and several leaders pop out of the crowd !

On our end, we announced two deals: our portfolio company Weecover raised a new round of funding to keep growing its embedded insurance offer in Spain and LatAm. Celest.Science raised a first round to bring its innovative climate risk model to the market in Europe and the US.

InsurTech was very active across Europe. Though the three largest startup ecosystems enjoyed various dynamics. Once again, Germany lagged behind with only 2 deals announced for a total of 16m€ raised. Both KPI are far from what happened in the UK and France, which led the wave for the first time in a while (in terms of deals announced).

But the ‘rest of Europe’ is worth a round of applause at it accounted for 35% of all deals announced in the first half of the year. This is among highest ranges in a while. And several ecosystems, usually more discreet, enjoyed funding rounds like Norway, Estonia, Romania or Hungary.

Last, but not least, half of all m&a deals announced in the first half of the year, were initiated by startups in the rest of Europe. Which confirms it’s worth having a look at insurance innovation way beyond one’s domestic market !

Subscribe to our newsletter:

First and foremost - following the switch in VC growth strategies from ‘growth at all costs’ to ‘profitable costs’ - several players announced they achieved break-even. The most famous one, Zego finally announced it is cash flow positive, which makes it the third European InsurTech unicorn to achieve it, after CLARK and Marshmallow . And beyond this shiny player, CyberDirekt in Germany and Mila in France reached profitability too.

As discussed and expected in a while, M&A deals happened once again. There were 6 acquisitions announced in the first half of this year, which is flat from the same period of time last year.

Nonetheless, the dynamic was slightly different and two deals pop out of the crowd: Guidewire Software acquired Quantee from Poland and Earnix acquired Zelros by Earnix from France (in ou portfolio !). Both have in common they were inked by non European players. And both were done with tech-first companies. Which makes them enthusiastic M&A deals, highlighting tech startups can indeed add value to the insurance industry and the European market is home to great players !

And beyond their domestic and European markets, startups are often looking at the US market to reach a new scale. In the first half of the year, there’s one player who confirmed its appetite for European InsurTech: Marcus Ryu. He is Guidewire’s co-founder and partner at Battery Ventures. As a VC, he invested in Descartes Underwriting, after a deal in hyperexponential - one of the largest round last year. In addition, Guidewire acquired Quantee in the first half of this year after it invested in it earlier, alongside other European startup: Friss, Shift Technology or Akur8.

First and foremost, insurance is no exception and AI is increasingly exploring how to revamp the industry. In that background, AI-first InsurTech accounted for 36% of all deals announced during the first half of the year.

As this is a major topic you are interested in - based on a survey we ran a few weeks ago - we’ll share a specific article next week, focusing on the dynamic in "AI in insurance".

Related to that trend is B2B. More startups are building technology for incumbents. Once again it accounted for close to half of all rounds announced (45%) which is higher than compared to the same period last year. And this raises questions among VC: are there as many pain to solve in insurance as there are B2B startups on the ground. Beyond the joke, this raises a concern on the value proposition as technology is just a means. While there are still room for innovation, sales cycles are so heavy in the insurance industry that revenues expected should be high enough to cover such investments. This means the value proposition should be strong enough to unlock significant revenues. In addition we see more startups coming closer to the insurance core engine: underwriting or pricing.

Finally, comes what we expect to be the next major wave of insurance innovation: emerging risks. On one hand, new risks are pilling and incumbents are increasingly releasing their own rankings of threats. If climate change and cyber threats are usually part of the top 3, there are many other challenges incumbents should get ready to tackle. They have all in common: a lack of historical data - meaning a lack of understanding - and a growing impact on insurers’ financials.

In that background we see more InsurTech players, tackling the ‘product’ part of the value chain. They are often tech-enabled MGA, meaning they rely on data and algorithms to cover specific verticals. In the first half of the year, that section was very active once again and 18% of all deals announced were in that category (compared to below 10% of all deals during the first wave of InsurTech). And ‘niche’ markets might be too small for incumbents but very nice opportunities for startups, which can add value by offering better tailored - or more fine-tuned - products to customers, thanks to new data sets or better algorithms. And in the first half of the year, this goes beyond climate and cyber, with maritime insurance or other specific commercial lines.

Last but not least, beyond pure InsurTech startups, we spotted players covering several industries, including insurance. These players are rather in the ‘resilience’ category, working on the broader risk value chain: at the prevention or mitigation level for instance. We enjoyed: Acoru, fighting financial scams ; Riot, preventing cyber threats ; OroraTech, fighting fires ; and Sword Health, preventing mental health. They are not InsurTech startups but a great examples of tech-first solutions that matter to the insurance industry.