March was once again very active!

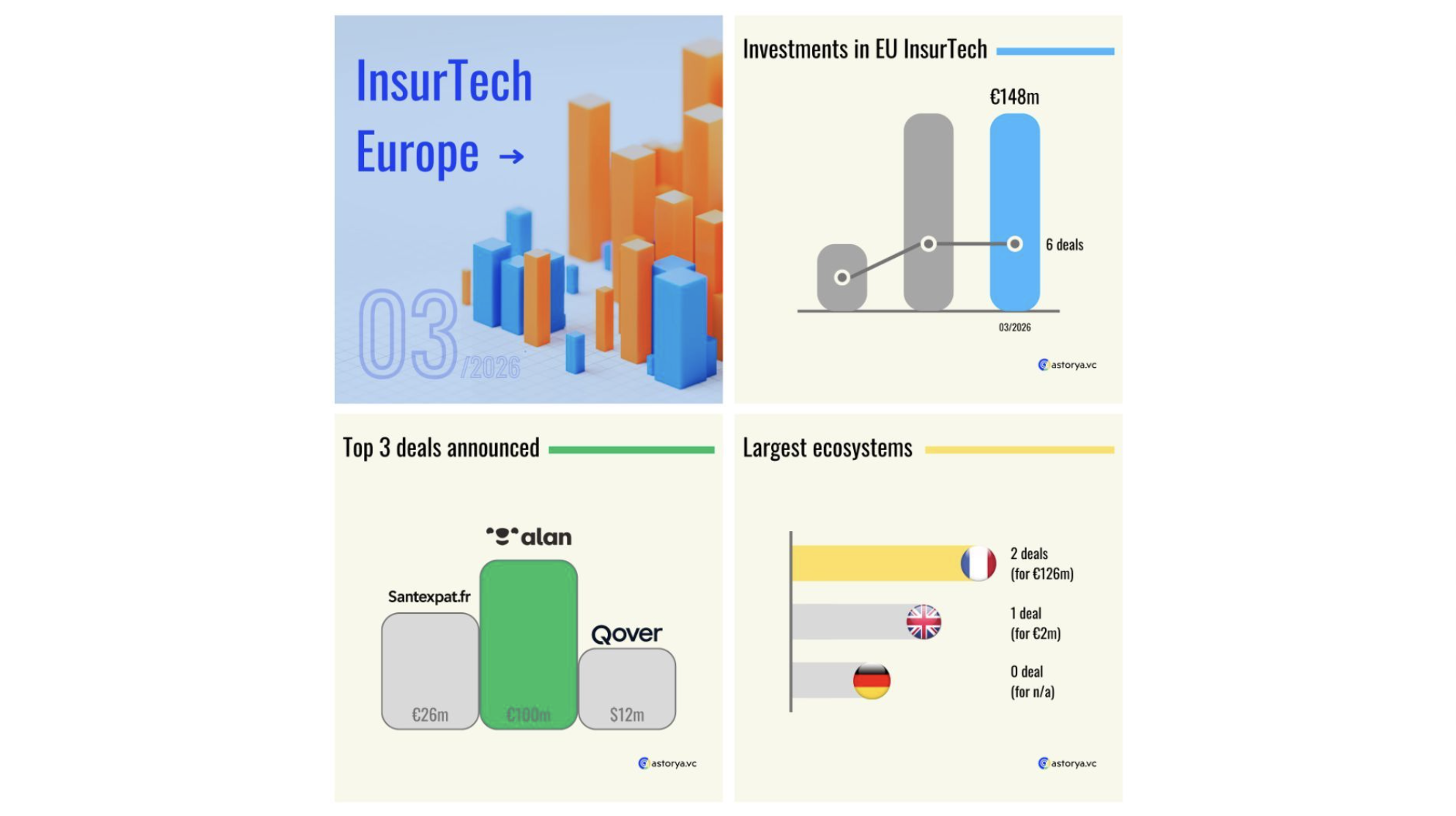

Indeed, six deals were made public over the past few weeks, in line with the previous month—and at the higher end of what we have seen in recent years.

At the end of the first quarter, we are now at +25% more deals announced compared to the same period last year!

But it is especially on the invested amounts side that this strong momentum becomes clear. Indeed, €148m was raised by startups innovating in insurance across Europe. The figure is identical to last month, which—if you remember—was already one of the highest in recent times.

Of course, we should not forget that a single deal alone accounts for €100m. But that is part of the “noise” (so to speak) of this KPI that is total invested capital. By definition, it depends on one or another mature player capable of raising nine-figure rounds! Still, behind that, another deal exceeded €20m raised, which remains significant in the current market.

Over the first quarter, more than €300m has been invested in European InsurTech—already as much as during the entire first half of last year. And we need to go back to 2022 to find a first quarter as strong in terms of capital raised!

Let’s also highlight, once again, the strong momentum coming from the “rest of Europe”—that is, outside the three major ecosystems of France, the UK, and Germany. Indeed, half of March’s deals were announced in these geographies, which now represent 40% of all deals since the beginning of the year—once again confirming how important it is to look beyond one’s domestic market, wherever you are based!

In short, 6 deals announced, for €148m invested—that’s what you need to remember on the numbers side.

Subscribe to our newsletter:

Let’s now take a closer look at the largest deal of the month, to better understand the company that illustrates the “category leader” trend mentioned earlier.

At the top of the podium is ALAN, which announced the largest round of the month. The French startup raised €100m in a new funding round led notably by one of its historical investors, Index Ventures, which doubled down alongside other existing backers. This round, described as opportunistic by the company, comes 18 months after a previous €180m round announced in September 2024. Since its launch, the startup has raised more than €750m in total and is now valued at €5bn, according to information disclosed during the latest round.

As a reminder, the company operates in the health insurance segment and has held an insurance license since its inception. Alan therefore belongs to the category of full-stack insurers. Since launch, it has targeted both SMEs and large corporates, and has recently won several tenders to cover operators linked to French ministries. It is also active in Spain, Belgium, and more recently Canada.

Beyond standard health insurance, Alan has stood out from the start thanks to its mobile application, which remains a benchmark with a 4.9/5 rating on iOS. It also offers a broader ecosystem of health services that complement insurance itself—a recurring theme among traditional players. The company has even introduced gamification features to promote prevention, encouraging users to walk more on a daily basis.

On the metrics side, as Alan recently celebrated its tenth anniversary, the startup reports profitability on the French market, with more than 1 million members covered across all its geographies. As of the end of 2025, it generates over €785m in annual recurring revenue.

At the time of the funding round, it employs more than 1,370 people, according to LinkedIn figures—up 20% year over year.