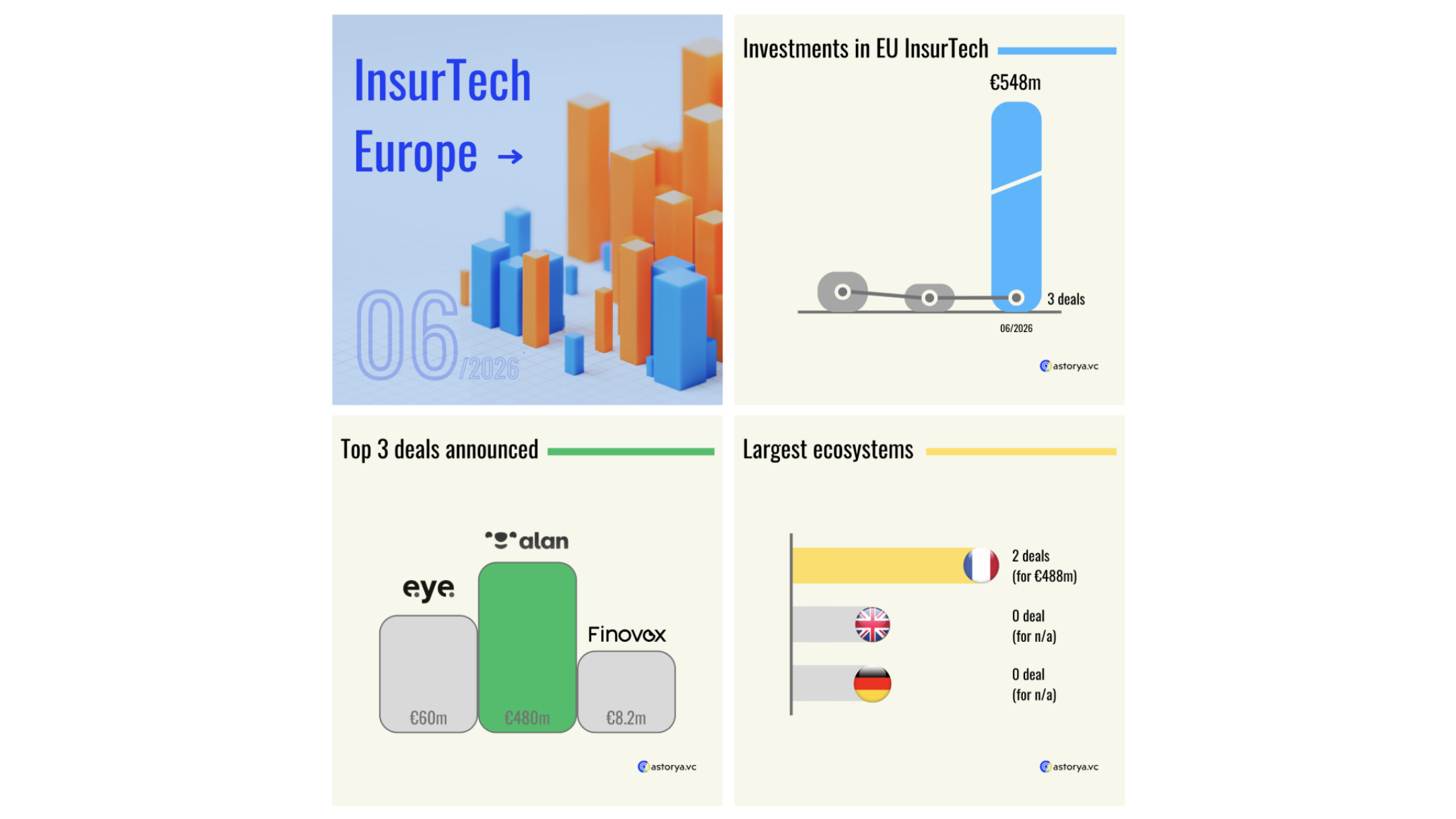

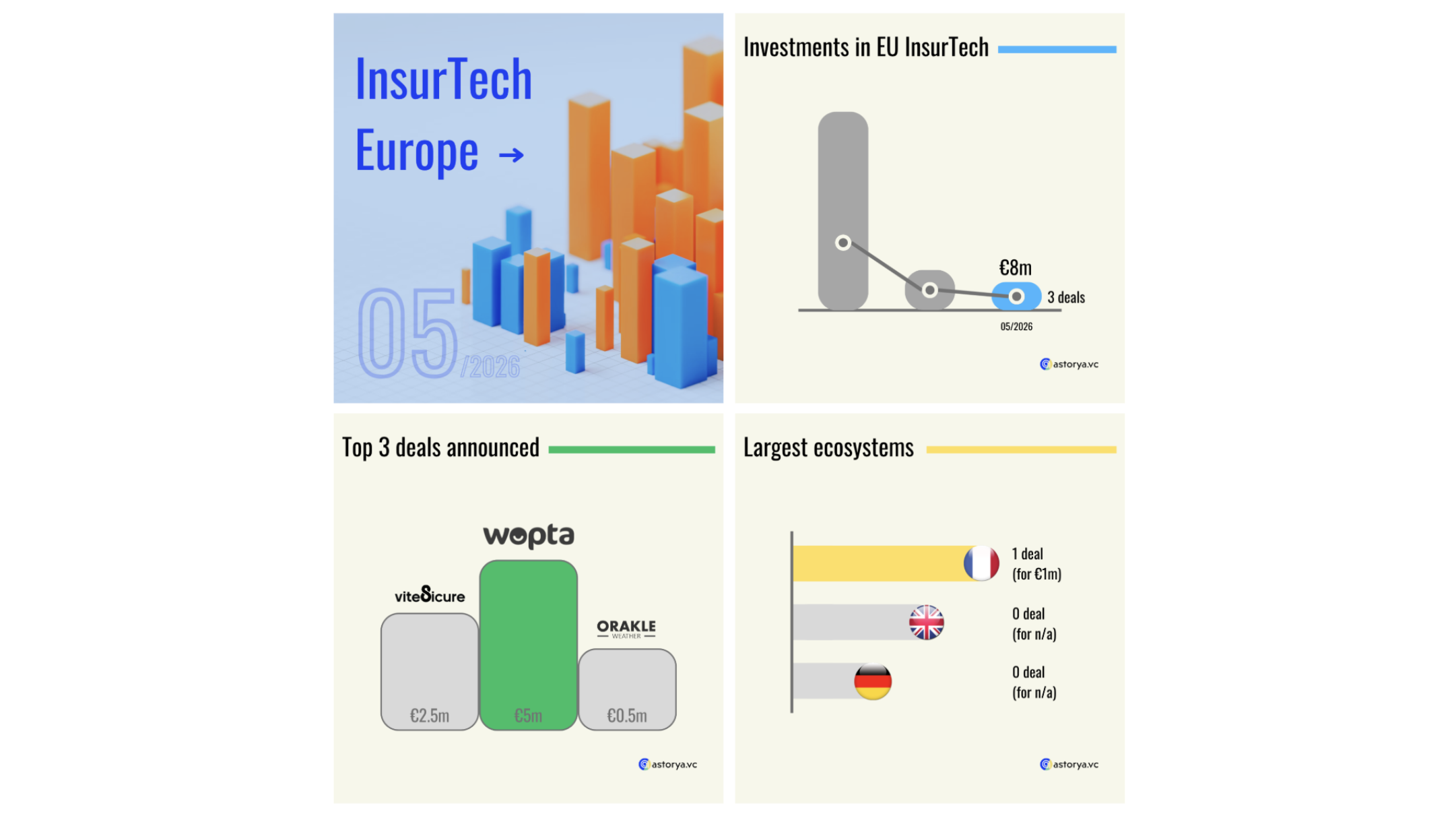

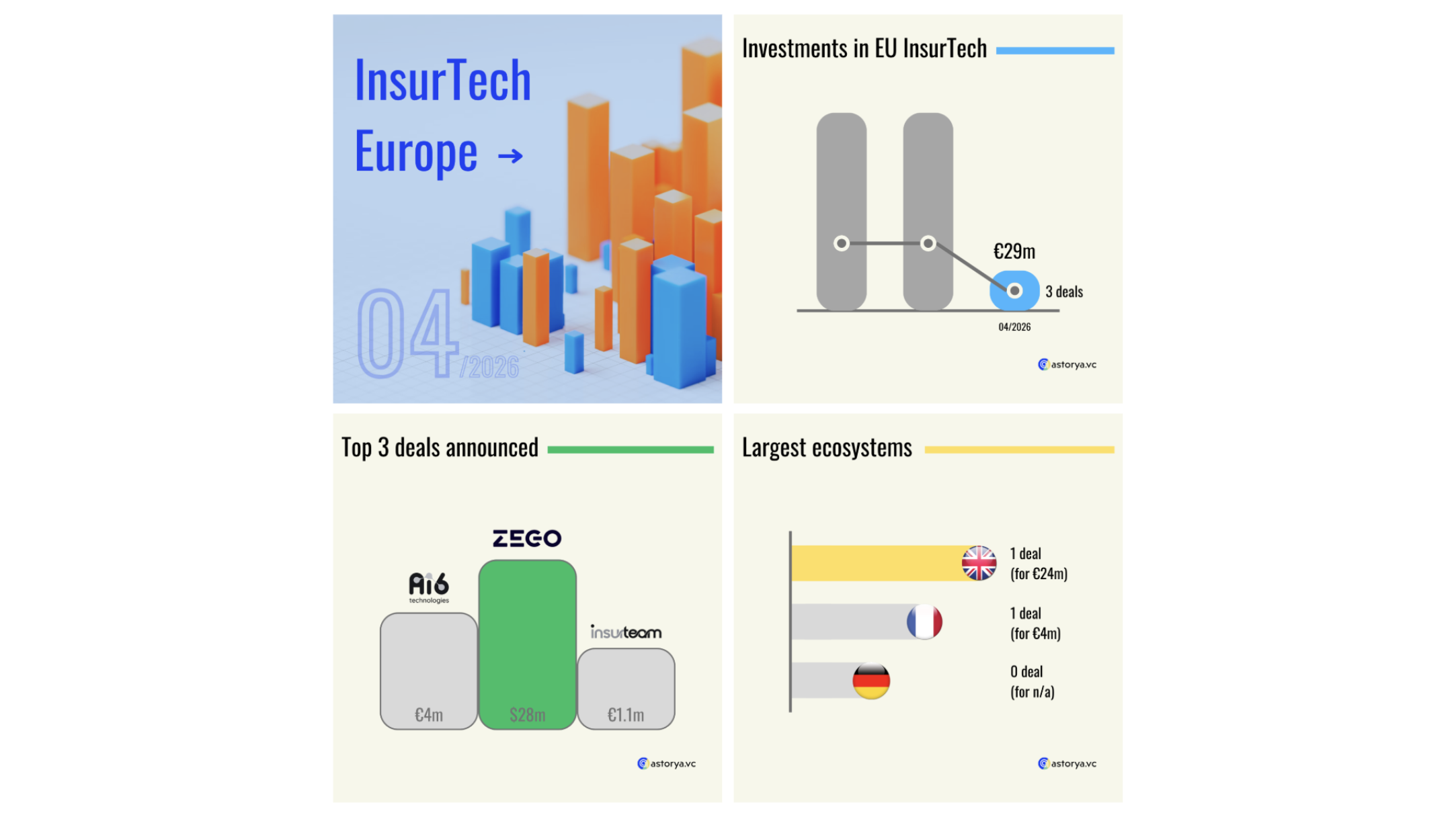

As the first quarter draws to a close, let's reflect on the investment landscape within the European InsurTech ecosystem.

A total of 17 deals were announced during this period, with startups securing a combined funding of €179 million. While the deal volume remains consistent with the previous year, the investment volume faced a slight decrease of -8% compared to the same period last year. This trend indicates a steady state of affairs, maintaining alignment with the industry's long-term trajectory, albeit below the peak observed in 2021-2022.

The biggest round was announced by Hyperexponential. This startup, based in the UK, focuses on the underwriting - in terms of pricing - part of the value chain. If you're used to our analyses, you know that this section has been rather quiet in terms of investment in recent years, despite several predictions of increasing activity from startups in this part of the chain. The announced round of $73 million is therefore quite unusual. Because in addition to its positioning, the amount raised is also out of the ordinary. By comparison, it would have been the second-largest ticket last year! Also noteworthy is the presence around the table of two iconic American investment funds: Battery Ventures and Andreessen Horowitz. Finally, it's interesting because this startup has experienced significant momentum judging by the evolution of its team: which increased by 30% in one year, when the European median has declined by: -7%!

The second largest deal was announced by Eye Security. This Dutch startup operates in the highly dynamic cyber-insurtech sector. Like many of its counterparts, it offers a solution that combines prevention tools, a distribution facilitation solution for brokers, and obviously a cyber insurance product. With this €36 million funding round, it remains ahead of similar startups offering a similar product. If 120 employees are listed on LinkedIn (up 46% over the past year), it is worth noting no figures on its current activity level were disclosed. JP Morgan Growth Equity is entering the company's capital as part of this financing round. The funding is intended to strengthen the startup's presence in its local market - the Netherlands - and in the German and Belgian markets where it already operates. Finally, the startup mentions plans for new country openings in the future.

Last but not least, Hellas Direct raised €30m. As a reminder, the Greek startup offers various personal insurance products online. It is possible to subscribe to car or home insurance on its website. It's worth noting that its initial positioning was exclusively related to car insurance. Note that its last funding round dates back to June 2021 and was similar in size at the time. The announcement of this new funding round comes with a clear commercial roadmap: aiming to strengthen its development in Central and Southern Europe. On this occasion, the online media Coverager indicates that the startup ended 2023 with 900,000 covered clients generating a total of €155 million in premiums.

Subscribe to our newsletter:

In terms of geography, the UK has once again emerged as the frontrunner, leading in both the quantity of deals unveiled and the capital injected into InsurTech startups. Nevertheless, it's noteworthy to underscore the substantial activity observed in "the rest of Europe," encompassing regions beyond the primary startup hubs. This ecosystem secured the second position in terms of both deal volume and investment volume. The specific rankings of France and Germany vary based on the criteria used to assess the dynamism of the sector (deal or investment volume).

In terms of business lines, the spectrum remained diverse, with all sectors receiving attention. However, there was a slight decrease in activity within the B2B sector compared to the previous year, constituting 29% of all deals announced during the first quarter (compared to almost 50% last year !)

Ultimately, the investment landscape across the value chain remained consistent with recent trends. 'Distribution' continued to dominate, comprising over half of all deals announced, although notable innovation trends are evident within this sector. 'Underwriting' experienced a resurgence after a period of relative quiet, while the 'product' segment of the value chain remained hot, particularly driven by startups addressing emerging risks.